The flipping of the calendar to a new year ushers in the usual look back, secure in the knowledge that we won’t be wrong about what transpired. This is almost always accompanied by a forecast of what’s expected in the year to come, which has only a passing or tangential connection to what will happen since no one has privileged access to the future and the future is not forecastable with any degree of granularity. The method most forecasters use is to believe that tomorrow will look pretty much like yesterday. Paul Samuelson, one of the 20th century’s greatest economists, was once asked how far into the future a good economist could forecast. He quipped: “One quarter back.” Forecasts are heavily influenced by the recent trajectory of events. A year ago, following the worst December for stocks since 1931, the outlook for 2019 was decidedly cautious and the great worry was that the global economy might be on the brink of recession, due in part to the Federal Reserve’s raising of interest rates. Few, if any, predicted a strong stock market given how bad the fourth quarter returns were. The result was the best stock market in years.

As 2019 drew to a close, the mood was quite different with stocks posting record high after record high. Still, the so-called “chattering classes,” those who make their living talking or writing about stocks but not by actually owning or managing them, evinced little enthusiasm. The worry about “irrational exuberance” that Fed Chairman Greenspan raised in 1996 was largely absent. I would characterize the mood as that favorite term of pundits, including those who actually do manage money: “cautiously optimistic.” This tepid bullish consensus was based on “one quarter back”: a rising stock market, growing profits, record buybacks, solid dividend growth, low inflation, stable short term rates, and a Fed that was injecting liquidity into the economy instead of withdrawing it. Equity valuations were higher than historical averages but quite reasonable given the inflation rate and the prevailing level of interest rates. There was a behavioral aspect operating here as well. The forecaster always sounds more serious and smarter if he or she is cautious and expresses concerns about the risks that are always lurking about, especially when stocks are at an all-time high.

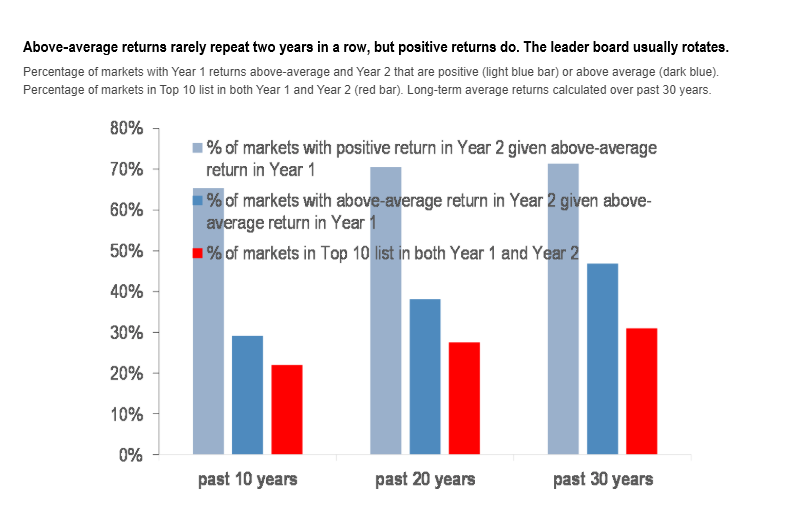

Then President Trump ordered a drone strike that killed Iranian general Qassem Soleimani, along with several other Iranian military leaders. Stocks promptly fell, bonds rose, as did oil and gold, all of which were perfectly sensible initial responses to that unexpected event. Not surprisingly, the mood of the pundits changed immediately. Barron’s 2020 outlook issue a few weeks ago surveyed market strategists and typified the cautiously optimistic view: a “more muted” 2020, with stocks rising 4% on average. Add in a 2% dividend yield and the expectation was for a 6% return. That is about as cautious as can be since, after an above-average return in stocks one year, there is about an 80% probability they are higher the next year. Over the past 30 years, the odds of both years being above average are about 50%. There is about a 30% chance both years will be among the 10 best of that period. Barron’s cover today (January 6th issue) is headlined “SAFETY FIRST” (all caps) and its highlighted stories are on how to protect gains, where to look for income and the outlook for oil and gas.

This immediate change of tone in response to a single unexpected event, which may or may not be negative, although the overwhelming consensus is that it is negative with comments ranging from “a game-changer” to “catastrophic” to “an act of war” being typical, is characteristic of this entire bull market since it began in the spring 2009 and is now the longest-running expansion and bull market in US history. The shock and trauma of the 2008 financial crisis were so scarring that people have been and remain risk and volatility-phobic and see every negative event as presaging a serious correction or perhaps a recession and bear market. As long as that attitude prevails, perceived risk will tend to be magnified and real risk will be less than perceived, which provides an opportunity for what Ben Graham called the “enterprising investor.”

Neither I nor anyone else knows what, if anything, will come of the attack on senior Iranian military officials. General Soleimani was reported to be the highest-ranking military officer in Iran and the country’s second most powerful official. Iran’s economy is in free fall due to US sanctions, its inflation rate is 40%, and the population is restive. The government reportedly killed hundreds of protestors in the past month who were seeking change. My point is the market has consistently overestimated the risks and underestimated the returns for the past 10 years. It is likely doing so again. As Justice Holmes once said in a riff on Ecclesiastes 9:11, “The race is not always to the swift, nor the battle to the strong, but that’s the way to bet.” (The quote is widely attributed so it may not have originated with Holmes.)

Stocks will not move in a straight line higher even if the bull market continues in 2020, as I believe it will. Setbacks and corrections should be expected, but unless something causes the economy to tip into recession and earnings and cash flows to decline, which I do not expect even if the geopolitical situation gets grimmer, then the path of least resistance for stocks remains as has been for a decade: higher.

Bill Miller, CFA

January 6, 2020

S&P 500 3246.28