As the Iran War moved towards a peace settlement, the marketplace celebrated by rushing back into longer duration equities. During Q2, momentum stocks led the equity market with one of the factor’s strongest quarterly returns, up more than 40%! As we highlighted in previous letters, there is significant overlap today between momentum, longer duration, and technology stocks. The S&P 500 Technology sector also had a strong quarter, +31.8%, more than double the S&P 500 return.

The AI-capex cycle remains robust, as major Hyperscalers’ capital expenditure plans increased during the quarter, estimated at greater than $2.5T from 2026-2028. The AI build-out will be one of the largest historical capital cycles; looking back at other large capital cycles, it is hard to predict future winners. The marketplace will eventually determine whether the appropriate ROI can be achieved to warrant the ongoing significant investment. The circular nature of capital raises, investment stakes and inter-connected revenue between industry players increases the risk of growing market excesses. Leading Hyperscalers have accumulated significant investments in leading AI private companies. As private companies aggressively raise capital to support the record investment, each round has seen significant increases in their market value and valuation multiples. As an example, Anthropic raised $30B of capital on February 12th at a $380M valuation only to raise another $65B on May 28th at a $965B valuation. The higher private AI valuations are also creating large private investment mark-to-market unrealized gains by public equity holders. This became more visible in the first quarter with some Hyperscalers showing a large portion of their quarterly profit being generated by updating the value of equity ownership in private companies.

Within the technology sector, the AI investment bottleneck shifted to semiconductors. The extraordinary demand has created record operating leverage and significant valuation expansion for the semiconductor stocks, up 112% to 258% during the quarter! The semiconductor industry has had a well-documented history of moving through boom-to-bust cycles – where excess demand/double ordering ends in excess supply and lower future pricing/profitability. During the Dot.com period, semiconductors peaked at a 7% weighting of the S&P 500 Index. Today, they are at a 19% weighting, nearly four times higher than 2022! The explosive growth in single name and sector momentum levered ETFs with significant exposure to technology and semiconductors are also fueling the growing concentration and valuation expansion. The marketplace is discounting that this time is different and peak margins and profitability will not follow historical cycles and continue well into the future.

The recent IPO market has also seen growing exuberance for longer duration equities. Some recent public offerings are at very high valuation multiples, with price-to-sales greater than 70x. Historically, IPOs at price-to-sales greater than 40x have significantly underperformed over the following three years. With recent IPOs at twice those valuation levels, it suggests extremely high marketplace expectations and limited competition are discounted well into the future.

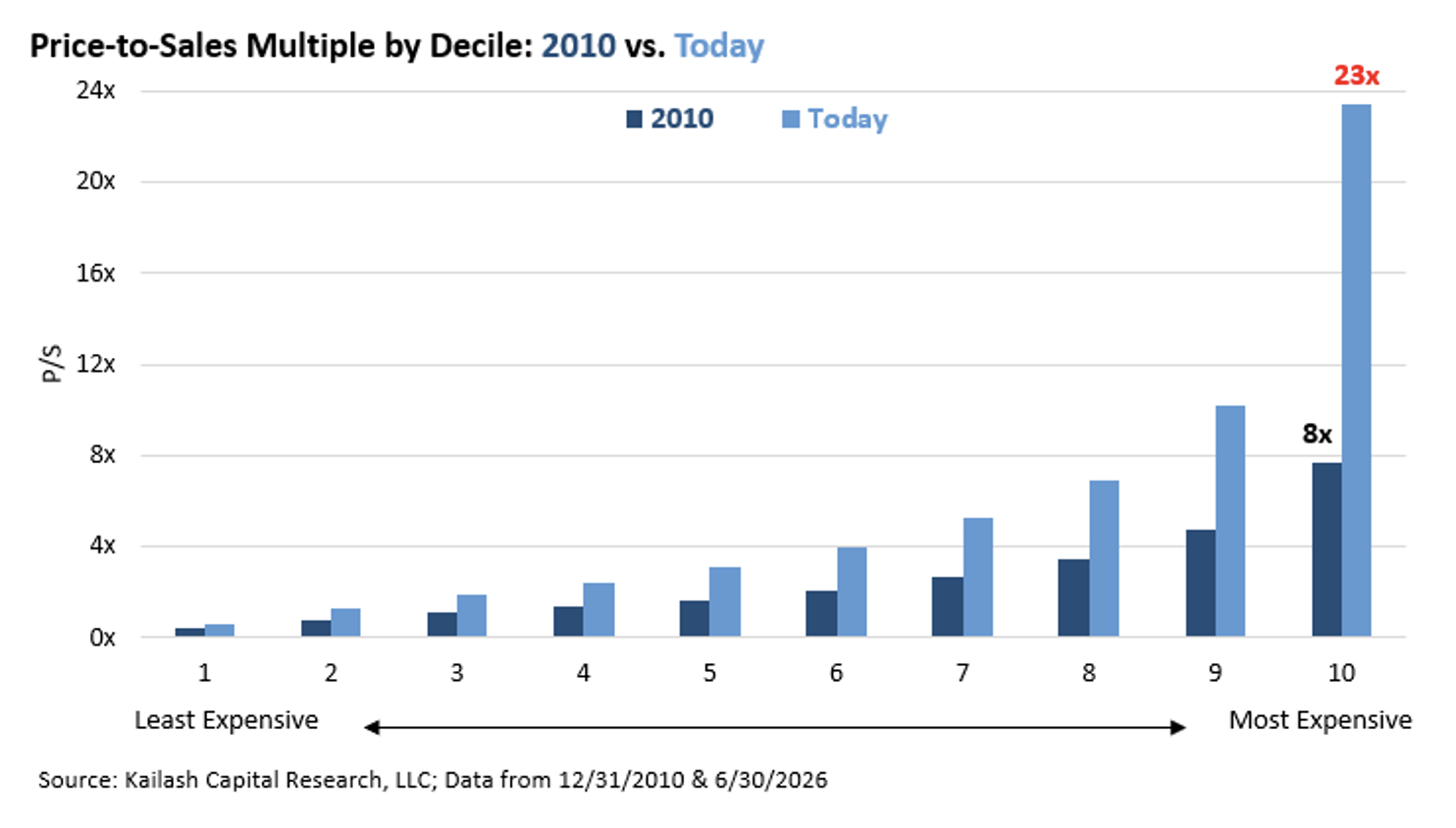

Today, price-to-earnings multiples may be underestimating valuation risk as an increasing number of companies are near peak margins and a growing amount of non-core earnings contributions. Other valuation measures show a clearer picture of valuation expansion among longer duration equities. The longest duration subset has seen their price-to-sales multiple expand to 23x, nearly 3x higher than 2010 levels, approaching 2021 peak levels, just prior to the long duration equity correction.

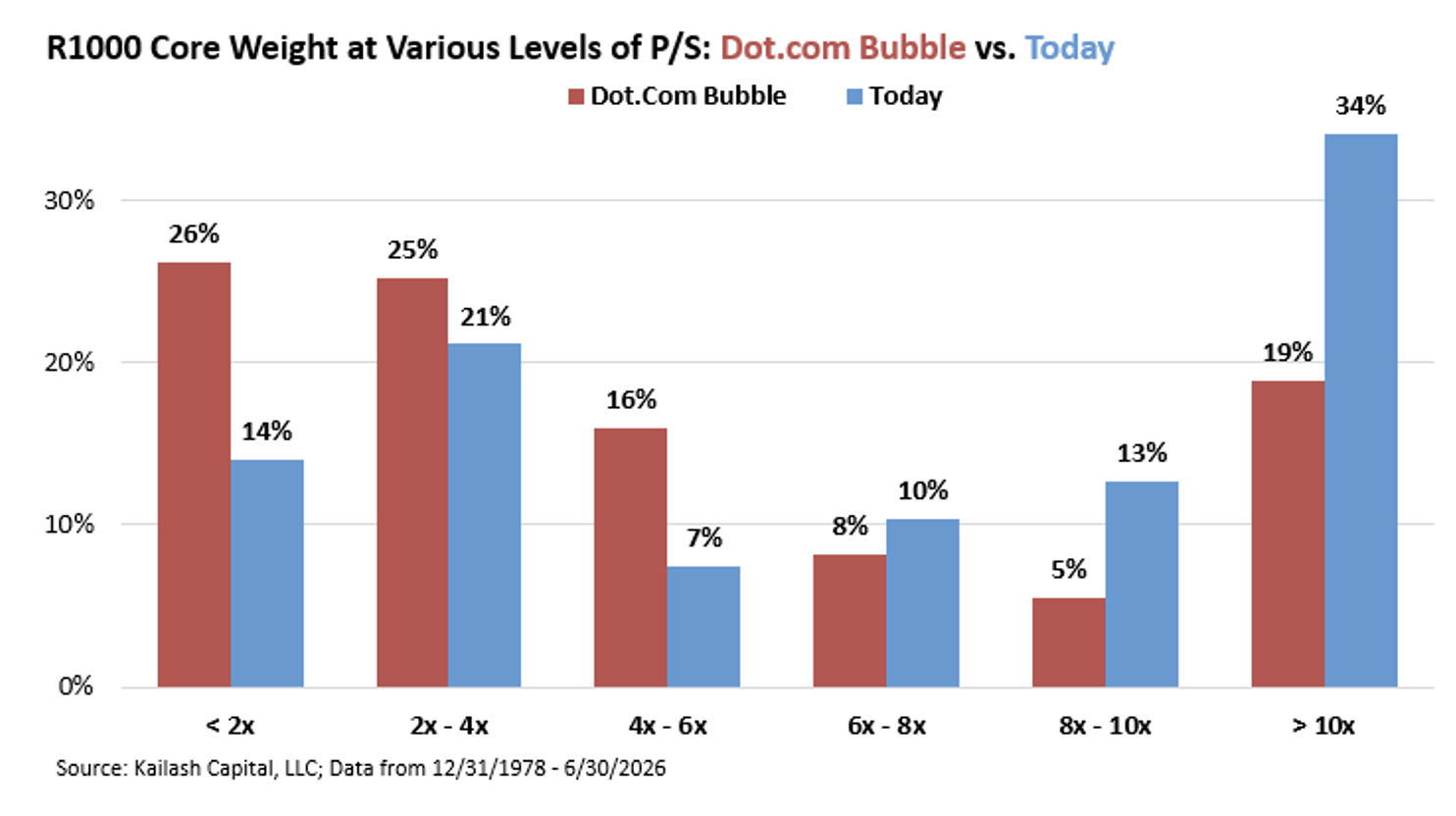

In addition, longer duration equities have significantly larger weights in passive broad indexes today versus the last major capex cycle (the Dot.Com bubble). Over the past quarter, companies in the Russell 1000 Core Index with a price-to-sales multiple greater than 10x increased from 20% to 34%, nearly double 2000 levels!

Given record concentration, wide valuation spreads, and growing long duration representation, risks continue to grow for passive indexes which could eventually become a headwind for future returns.

In the current bifurcated marketplace, we still see attractive value opportunities. Lower valuation securities have not seen significant valuation expansion or crowding due to their lower weightings in passive indexes and ETFs. Today, you can still find numerous overlooked companies with double-digit earnings and free cash flow yields, more than double the overall equity market’s yields and the 10-year bond yield. In many instances, these companies may be long-term beneficiaries of the AI investment cycle, increasing their margins and earnings through productivity improvements. There are very attractive reward/risk investments beyond the crowded AI companies with high embedded expectations.

A broadening of the market over time could benefit lower valuation and smaller market caps. While smaller market caps have had a good start to the year, we still see significant opportunity for a multi-year outperformance cycle. Small cap value stocks remain at record valuation discounts to larger companies with improving relative earning growth.

Not surprisingly, they remain under owned and under followed. Sell-side analyst coverage of smaller market caps has reduced significantly over the past twenty years. Today, it is common to find only 1 to 2 analysts covering out-of-favor $1B market cap companies. Meanwhile, the top 7 companies in the market are covered by an average of 56 analysts, with more than 80% having a Buy rating. Smaller market caps present a less efficient marketplace where an investor has the potential to uncover significantly mispriced securities, providing an opportunity to buy ownership stakes at a fraction of their long-term fundamental value. With valuation levels near historical highs, longer duration equities have embedded high market expectations and low-single-digit or negative free cash flow yields and growing risk of potential future capital loss. We see the opposite environment within the lower valuation small cap universe – investment opportunities with multiple long-term value drivers, accelerating earnings and free cash flow, earnings and free cash flow yields multiples above the overall market, future valuation expansion potential, and equity accretive capital allocation opportunities.

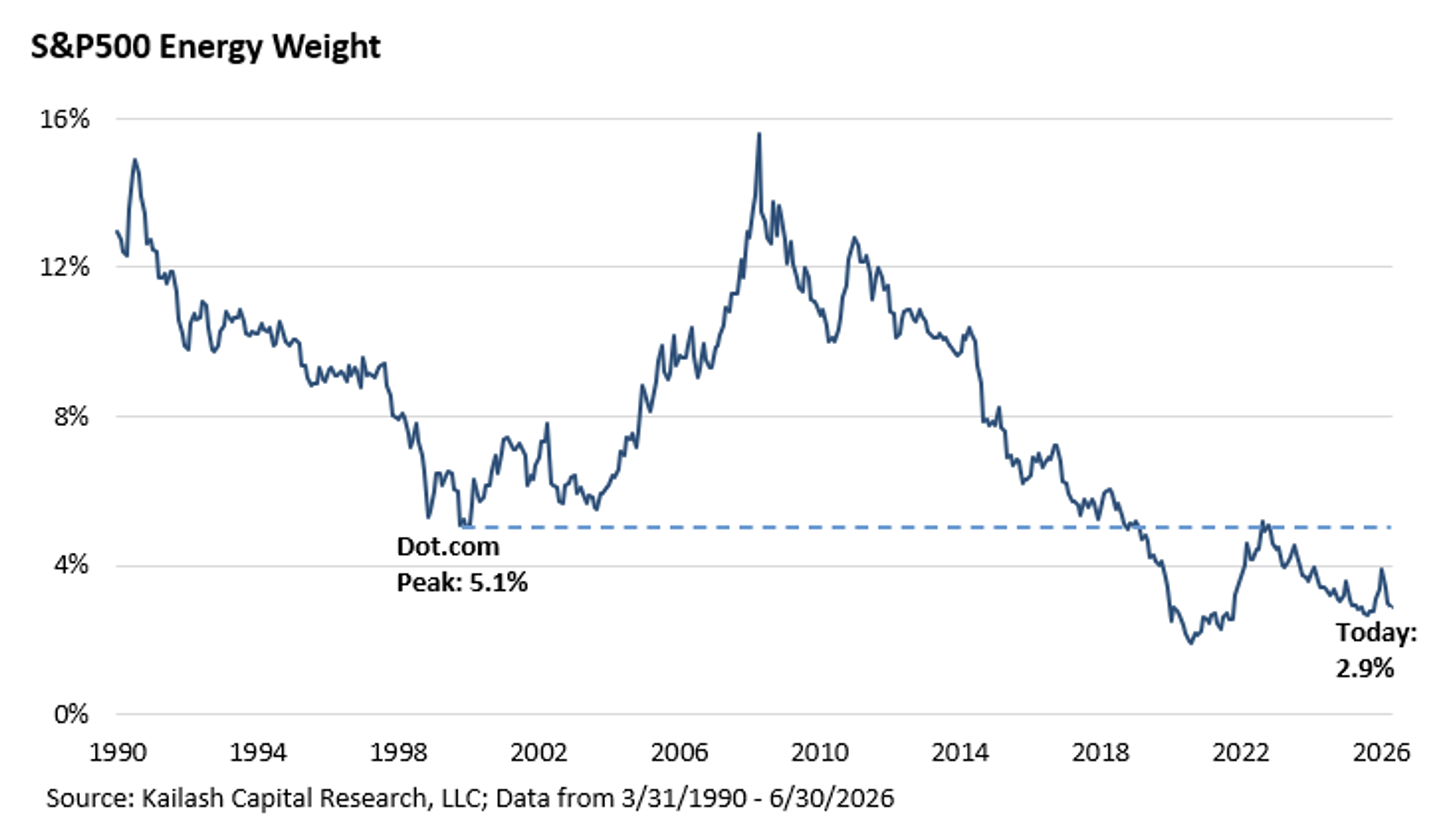

As an example, the Energy sector underperformed during the second quarter with the announcement of an Iran ceasefire. At the end of the quarter, S&P Energy sector weight was back below 3%, near the end of 2025 and not far from 2021 levels (which was a 35-year low). However, the industry fundamentals today are more favorable than those time periods.

The oil forward curve is $10/barrel higher than at the end of last year. Energy company balance sheets have significantly improved from the 2020-21 trough period. The supply/demand environment is more favorable with production facilities in the Middle East below pre-war levels. We currently see some great investment opportunities, trading under 2x cash flows, with no near-term debt maturities, capital structure trading at or above par, 20%+ earnings and free cash flow yields, and, in some cases, dividend yields approaching 5%. Similar to the 2021 lows, there is a nice set-up for Energy equities: low expectations, market prices well below fundamental values, and a lack of ownership given low passive index weightings.

With the marketplace favoring momentum and longer duration equities, we believe lower valuation and smaller market caps provide attractive long-term return potential.

Deep Value Select Strategy Highlights

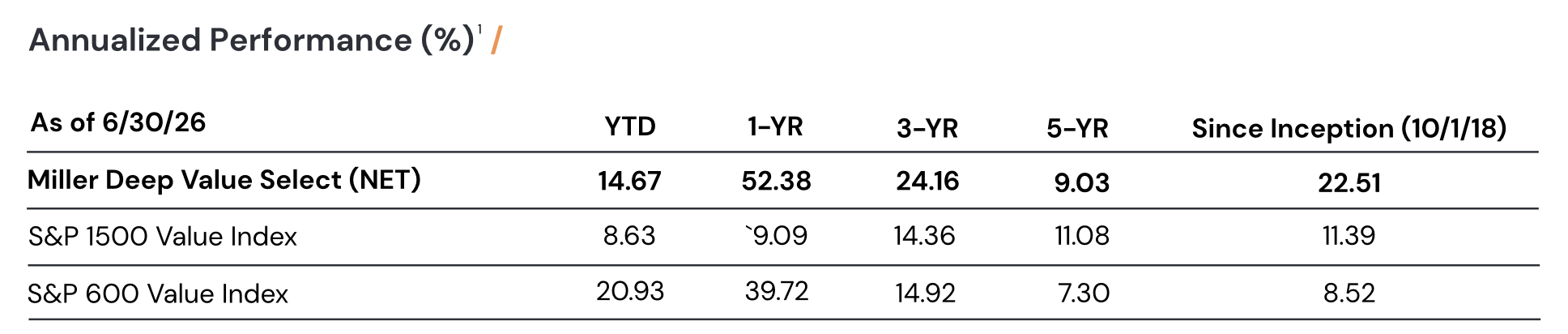

During the quarter, Deep Value Select was up 5.80% (net of fees), though behind the S&P 1500 Value Index’s 8.42% and the S&P 600 Value Index’s 15.93%. For the first half of the year, Deep Value Select was up 14.67% (net of fees) versus S&P 1500 Value 8.63% and behind S&P 600 Value 20.93%. While the Strategy has generated strong first half performance, its near-term performance experienced some headwinds from our investments in the energy sector and one of our investments in the communications sector.

During the quarter, the largest positive contributor was Bloomin Brands (BLMN), whose share price rose 66.7%. The company is in the midst of a multi-year transformation, and new menu changes at Outback with a greater focus on food quality are showing up in improving consumer scores. Restaurant traffic showed directional improvement last quarter and is expected to continue to improve over the coming quarters. For the remainder of the year, management is investing in the business, enhancing the service experience, accelerating restaurant remodels and new marketing initiatives. Success of the transformation plan is expected to drive Bloomin Brands restaurant banners back to consistent positive comps and lead to margin improvements over the next couple of years. The company is near historical low 7-8% EBITDA margins versus industry peers in the low- to mid-teens. In terms of risk, investments to drive future revenue improvement will be a near-term headwind to margins as well as higher beef costs. However, Bloomin Brands share price appears to discount a significant portion of these concerns, embedding no future success from the transformation plan. The company valuation is near historical trough levels and a significant discount to peers, price-to-sales near 0.2x, forward EV/EBITDA below 5x and normalized earnings yield greater than 30%. Based on our analysis, success on the transformation could result in normalized EBITDA >$500M and, with only $60M of long-term maintenance capex, a normalized annual free cash flow yield >40%. If the transformation succeeds, we believe Bloomin Brands could have substantial long-term upside from the current share price.

Our two largest detractors during the quarter were Crescent Energy (CRGY) and Gray Media (GTN), whose share prices declined 21.9% and 7.6%, respectively. Both companies’ share prices are at deep discounts to what we believe is their long-term fundamental value, and we have recently increased our positions in both holdings.

Crescent Energy (CRGY) stock price has recently pulled back as the price of oil has fallen with progress on ending the Iran conflict. We believe the share price pullback is a significant opportunity given Crescent’s numerous value drivers that have potential to unlock equity value over time. The recently completed Vital Energy acquisition provides attractive merger synergies to accelerate debt reduction, but, more importantly, it expands Crescent’s production footprint into the Permian Basin. A new senior executive who successfully built Pioneer’s Permian extensive asset base will lead Crescent’s effort, providing an attractive long-term growth opportunity. Management has also successfully built a mineral asset and royalty business that generates $200M of annual EBITDA. Current private and public mineral transactions have been at 7-11x EBITDA multiples which suggest significant $1.4-$2B+ of underlying value. With acquisitions as a core part of the long-term strategy, there will always be risk of merger challenges. However, management has been very successful in acquiring assets over the past 10 years and their underwriting is done with conservatism focusing on quick payback and accretion to free cash flow and NAV. Based on our analysis, even with the recent pullback in energy prices, Crescent could be well positioned to deliver $1B+ in annual free cash flow over the next several years. Crescent shares remain very attractive, below 2x cash flow, 30% forward free cash flow yield and an attractive 5% dividend yield.

Gray Media has lagged the Strategy, as core advertising has been weaker recently due spending pull back as a result of the Iran war and uncertainty related to a Supreme Court ruling on political advertising. Gray is positioned to benefit from the FTC’s efforts to modernize industry regulations, as the company has recently completed a series of small tuck-in acquisitions. The recent transactions have created more than 10 market duopolies, supporting attractive future synergies and balance sheet accretion. While the recent Supreme Court ruling allows greater use of the lowest rate for other political advertisers, it eliminates the advertising cap which could increase overall spending for the upcoming mid-term elections. While political advertising is difficult to forecast, Gray’s #1/#2 ranked stations in 89% of their Neilsen measured markets make the company well positioned to benefit from close races and generate in the neighborhood of $400M+ of political advertising during the back half of the year. While the company has higher debt leverage, Gray has substantial liquidity and has no debt maturities before 2029. Marketplace expectations for Gray’s future retransmission revenues remain very low, also providing a nice ongoing variant as management focuses on improving their long-term retransmission agreements. Near-term risk remains an advertising recession; auto advertising may be weaker over the coming months but there is potential improvement over the next 6 to 12 months. Based on our analysis, Gray has the potential to deliver strong free cash flow over the coming quarters and $2B+ over the coming 5 to 7 years. Ongoing debt reduction should accrue to the equity over time, and we see very attractive long-term upside potential.

During the quarter, we initiated a position in Coty (COTY), a significantly mispriced consumer beauty company in the midst of a multi-year turnaround. Coty’s crown jewel is their prestige business which has a leading, vertically integrated, global fragrance platform. Their prestige segment makes up two-thirds of the company’s revenue and 90% of the company’s profit. Over the past five years, the company has strengthened its fragrance innovation, revamped its Consumer Beauty division, modernized their innovation pipeline and significantly de-levered the company balance sheet from more than 6x leverage to less than 3x today. However, prior management’s focus on smaller new brand innovation and a sell-in oriented business model led to consistently missing financial results as excess inventory and product returns hurt profitability. Late last year, a new CEO with extensive transformation experience growing P&G’s Beauty business joined Coty. He is enhancing the turnaround plan focusing on more innovation on major brands, eliminating non-core business activity, increasing media and marketing on core brands, changing the business model from a sell-in to a sell-out approach, and working closely with their leading retail partners. While Coty’s transformations will take time to develop as near-term results will see some transition headwinds, we believe shifting the business model to a sell-out focus is the right long-term approach to unlock long-term value. With Coty’s share price more than 80% below its 52-week high, the small market cap does not reflect the significant company asset base (>$10B) and business model (revenue of >$5B). Coty valuation multiples are at a massive discount to peers and near all-time lows: price-to-sales of 0.3x versus peers at 2 to 4x, price-to-earnings FY2 near 6x versus peers at 19 to 26x, and forward EV/EBITDA under 6x versus peers at 10 to 16x. Success of the transformation could support substantial long-term upside from the current price.

We believe Deep Value Select offers clients a unique strategy, concentrated investments in multi-year transformation/turnarounds and mispriced cyclicals. Since inception, investments which generated more than 80% of the Strategy’s historical performance are no longer owned. We have recycled capital from mostly successful investments into new holdings or increased positions in holdings that have lagged Strategy historical performance. We remain excited about the current portfolio, as we believe the breadth and attractiveness of the current opportunity set are near the high end of what we have observed since the Strategy’s inception.

We thank our clients for their long-term partnership.

Dan Lysik, CFA

July 13, 2026

Stay connected with us for updates and insights. Subscribe.

Follow us here, here and here.